5 catalysts for company X – in short form:

- US Section 232. First steel and aluminum – uranium next?

- Modest valuation compared to US peers while having superior near-term production capacity.

- Potential other sources of revenue from vanadium and clean up work for the government of old US uranium mines that were never restored.

- There has been forced selling of shares from the uranium ETF Ura Global X for the past three months. This will slow down and stop completely by July 31st.

- Inclusion in the Russel 3000 index on June 25th = forced buying from institutions and small cap ETFs. News from yesterday.

So company X = Energy Fuels. This is a company which I’ve been accumulating from the end of March till now to a degree where it has now become my largest position in the uranium space so I thought I’d write a few words about why this is my #1 pick currently.

Note that this post will be a company specific post and not about the uranium sector. I made two videos on my view on uranium here: The Case for Uranium Part 1 and The Case for Uranium Part 2 in case you are interested in a deeper dive into that. Both were made before I started accumulating Energy Fuels (EF). My general view on uranium is unchanged since then if not slightly more bullish as hedge funds have started to enter the space buying physical uranium realizing that the industry is now on its knees so severely that supply destruction has become an economic necessity = uranium prices must rise. As always in cyclical industries where demand is certain: After rain comes sun.

A word of warning

Before I elaborate more on the 5 catalysts let me stress that EF (ticker symbol: UUUU) is an aggressive pick that comes with a certain amount of risk. I have personally chosen to size more heavily than I am normally comfortable with in relation to the amount of risk the stock carries with it because I see huge potential within a 1-year time frame. But realize that my uranium outlook is a lot more bullish than that of the general market, and even among uranium bulls. If I am proven wrong on the timeframe there are better uranium stocks available, specifically Uranium Participation where I’d postulate that the risk is almost insignificant and a 2x on one’s money in a three year time span extremely likely.

Note that if U3O8 prices stay below 45 USD/lb for the coming 12-months it is likely EF will need more capital as they have no long-term contracts and would sell at a loss at current prices. This could potentially lead to bankruptcy, but much more likely a dilutive capital raise. Neither option is ideal for investors but that is the price one pays for the significant upside potential.

Now for an elaboration of the above mentioned catalysts.

The 5 catalysts – in elaborated form:

- US Section 232. EF has tremendous upside if the Trump administration decides to help out US producers by forcing US uranium buyers to buy a 25% quota domestically (12 million pounds out of 180 Mlb of global demand = limited impact on the overall market).This could result in a two tier pricing system where US producers receive up to 30 USD per pound of U3O8 more than non-US producers = 55-60 USD/lb. Were that to happen EF would go up at least 3x and probably more.According to my calculations Energy Fuels EBIT at a U3O8 price of 60 USD/lb will be about 90-110 MUSD when ramped up fully (assuming 5 Mlb of production). Current share price of 2,06 USD = market cap of 150 MUSD.This may appear to be a long shot on the surface as it seems to go against the very soul of America. However, it has been in place before and many in the industry believe this to be a very real possibility and judging from that I’d say the chance is at least 30%.

The reason for all this speculation is that Energy Fuels and Ur-Energy sent a so-called 232 petition to the US Department of Commerce on January 15th claiming unfair competition from state-owned players in Kazakhstan much like the petition that the steel and aluminum industry submitted in the summer of 2017 and which the administration have now acted on in 2018. The argument is that subsidized players can afford to dump prices whereas others cannot and this leads to elimination of competition on unfair grounds.

Section 232 of the Trade Expansion Act in 1962 focuses on national security and for that reason the administration can act without support from congress. And since uranium is much more of a national security concern than steel and aluminum (20% of US electricity comes from nuclear energy) one might conclude that the administration is likely to act on it.

However, if national security isn’t the real motivation behind the steel and aluminum tariffs but instead it is jobs for American workers then uranium may not get the same backing as the new jobs it would provide are in states where the republicans are already dominating (Wyoming, Texas) and where they don’t really need the extra votes.

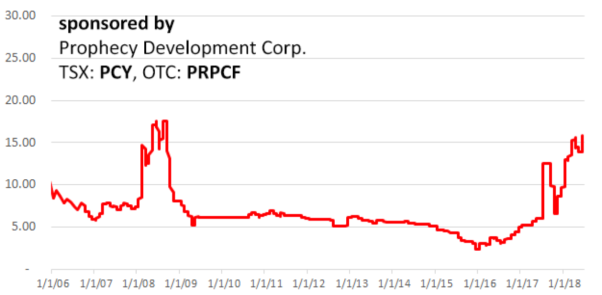

Note that there is a risk the stock will fall if the administration decides not to act. EF has outperformed the general uranium market the last three months and much of that could be due to investors beginning to price in the possibility of 232. The flip side to that argument is that the petition was submitted on Jan 15th and as can be gleaned from the graph below the response initially was not only muted but even negative.

And while we’re at it let’s include a graph for the last 5 years to illustrate the suffering that has been going on for shareholders (the general direction is similar for all other uranium producers):

- Modest valuation. EF can bring on more U3O8 in production in a shorter amount of time than the two other main US players, UEC and Ur-Energy, despite being valued significantly lower (close to 0,5x!) on an Enterprise Value to pounds in the ground basis. Because of those factors EF has significantly more upside.Why do I single out UEC and Ur-Energy specifically? Because they will also be affected by petition 232 (if you are in uranium for that specifically and want a US producer) and because all three have similar mining methods and mining costs (which are in the lower 2nd quadrant globally). This means all three can bring on production faster than most global competitors, which is why I believe that in the current environment this is where to look primarily. EF can potentially bring those costs even lower than the others, see catalyst 3.On the flip side, EF has higher overhead costs due to a bigger operation and a dilutive capital raise is likely to hit EF shareholders harder than those of UEC and Ur-Energy. UEC has a nice titanium deposit that potentially is worth a lot of money and Ur-Energy has some long-term contracts that go into 2021 whereas the two others have no existing contracts beyond 2018. In terms of current shareholder base rating EF would come in last of the three. That could change as a new management have been in place since January. My impression is that it is a more alert one.

Summary: If you believe that crunch time is very close EF is the play of the three imo. If you believe it happens in 1-3 years, Ur-Energy and UEC may be better options. If you don’t believe any of that stay out for now!

- Unlike most uranium companies, EF has other potential sources of income from vanadium and clean up work of old US uranium mines from the 1950s era when environmental considerations weren’t the same as they are now. Both are new opportunities that did not exist one year ago.The US government has set aside significant amounts of cash in the recent budget for clean up work of these old non-restored mines and it is my understanding that Energy Fuels is in a prime position to receive much of this work because of their White Mesa mill which sits close by.They also have vanadium in the ponds at White Mesa which they are now looking to extract as vanadium has shot up in price this past year. See graph:

On top of that EF can knock off about 10 USD/lb of U3O8 costs per pound from bi-product vanadium on some of their conventional mine production (which is set to come on at U3O8 prices of 60 USD/lb) if vanadium prices stay where they are. That means it could potentially come on sooner, perhaps at 50 USD/lb. UEC also has conventional mines with vanadium but it is my understanding that permits are years away for those.Both of these potential revenue streams can turn out to be of extreme importance to shareholders should uranium prices remain subdued for longer as new capital may not be needed. Note that both are in the ”if” category still though. We don’t know for sure if they will make a dime on either.

And two short term tactical triggers:

- The Uranium ETF Ura Global X is transitioning to go from 100% uranium producers to 70% uranium producers and 30% ”nuclear components”. This change started in March and the transition will be complete on July 31st. This means the ETF has had to sell 30% of it’s holdings in many producers.I started tracking their EF holdings from April 6th and the share count was then at 9,3 million. As of today this number is now 6,5 million = 30%. So that means the selling ought to stop if not shortly then at least by the end of July.Interesting to note that the EF share price has held up well in that period rising 35% despite the heavy selling. Ura Global X has been selling about 60,000 shares daily in the last two-three months. Considering the average daily volume in EF is around 500,000 this is a significant amount of downside pressure that is soon to be removed. Will the effect be like that of a bathing ball under water?

- Russel 3000 index inclusion. Yesterday EF announced it will be included in the Russel 3000 index from June 25th. This may lead to institutional buying propping up the price. However, there is some chance speculators have already anticipated this and bought ahead of time making the effect of the inclusion less significant. We’ll see.

I’d be interested in your view. All feedback is welcome. (And please excuse the formatting. For some reason spaces and paragraphs are getting messed up in this article even after being corrected).

On valuation – some numbers

Energy Fuels

Stock ticker: UUUU

Stock Price: 2,06 USD

Enterprise Value: 180 MUSD

U3O8 resources: 130 Mlb (EV/Res = 1,38)

Near-term annual production potential: 5 Mlb annually. (2,5 Mlb at 45 USD/lb + 2,5 Mlb at 60 USD/lb)

Annual Burn Rate: 30 MUSD.

Net Working Capital: 43 MUSD.

Interestingly: According to my calculations U3O8 prices at 45 USD/lb means Energy Fuels EBIT is at 10 MUSD, ie. barely above break even. However, at 60 USD/lb EBIT is around 90 MUSD (110 MUSD if vanadium prices stay where they are at now). This goes to shows the leverage that is at play here.

UEC

Stock Ticker: UEC

Stock Price: 1,56 USD

Enterprise Value: 255 MUSD

U3O8 Resources: 112 Mlb (EV/Res = 2,28)

Near-term annual production potential: 4 Mlb annually. (2 Mlb at 45 USD/lb + 2 Mlb at 50 USD/lb but the later cannot be brought into production till at least 2 years out)

Annual Burn Rate: 20 MUSD

Ur-Energy

Stock Ticker: URG

Stock Price: 0,70 USD

Enterprise Value: 95 MUSD

U3O8 Resources: 42 Mlb (EV/Resource = 2,26)

Near-term annual production potential: 2 Mlb annually. (1 Mlb at 45 USD/lb + 1 Mlb at 60 USD/lb)

Annual Burn Rate: Doesn’t apply due to long-term contracts.

Disclaimer

I do not accept responsibility for losses that are a result of buy/sell recommendations I make. I encourage you to do your own reserarch before making an investment decision.

IF the uranium price would reach previous highs of ~130$, is it possible Energy fuels could go x100 like it did in 07 or is the company different in some way compared to 07 as one could not hope for those massive returns?

LikeLike

That’s a good question, Carl. It’s a very different company now. Much more mature and many of the assets have been producing so in that way there are less question marks surrounding it and therefore the risk ought to be lower.

Suppose 130$ on a sustained level (which I don’t believe unless China all of a sudden decides to ramp up it’s nuclear fleet on a massive scale) Energy Fuels could earn in excess of 600 MUSD per year before interest and tax. If the market believed this to be a sustained U3O8 price, which again I don’t, EF could trade 25-50x higher.

A price around 80$ on a sustainable basis is not at all unrealistic, though it seems so right now given the current U3O8 price. If that was the case my estimate is that EF could earn around 200 MUSD before interest and tax plus the added benefit of having additional reserves 4+ years out. 10-15x wouldn’t be unreasonable in that case imo.

LikeLike

Thanks for the comprehensive answer! I’m liking what i’ve read so far on Energy fuels, gonna do some more reading during the weekend but i have a feeling i will make this my primary bet for the (hopefully) upturn in uranium. Question is if the URA rebalacing will put pressure on the stock as they seem to still have a lot of shares left to sell? Maybe one can hope for a near term block trade. Another company that at first glance look interesting is Forsys Metals, anything you’ve looked at?

LikeLike

Energy Fuels looks like a very compelling stock. If you look at some other equities in the space, they move up and they aren’t even producing anything. Isn’t that strange? I can’t say for sure, but I think that Energy Fuels will keep producing. They got alternate feeds and should keep making cash flow. Am hoping for a continued move up in stock price, because of their other cash flow operations and from producing uranium. There is risk in these equities but Energy Fuels, being the dominant producer in the u.s. And because they got the only conventional uranium mill in the u.s that can produce vanadium, copper, uranium and alternate feeds.

It should do well in a good market but do less bad in this market. The stock could have bottomed out before and as it’s like doubled now, looks good. I am thinking of adding more shares if the stock is to dip.. Anyone that knows something about uranium stocks should know that it’s like a rare opportunity if you can time it right. And could make 10x returns and maybe more.

However, we don’t know the result of 232 petition yet and as the stock market is at all time high levels, is something to keep in mind. Am just hoping the u.s administration will see that u.s producers would benefit from more supply to u.s utilities if they are to keep a uranium mining industry.

LikeLike

Nice work hammer. Thorough and thoughtful.

LikeLike

Thank you, Mike! Means a lot coming from you.

LikeLike

Many thanks for your work here…was curious if you have done any work on the EF former CEO’s venture Western Uranium ($wstrf)? Glasier appears to have put the pieces together to be ‘another EY’ once prices recover, fourth largest Uranium resource base with a fully permitted mill in the roadmap…while more risk is involved/they will only bring all this on steam at higher price points, it’s less than 1/10th the EF mkt cap…thots?

LikeLike

Been in since URZ……great buying opportunity earlier this year. Patiently waiting…..for all the reasons listed!

LikeLike

Good analysis, I’m with You on this short term investment thesis. I’m more concerned about uranium longterm (5+ years), since nuclear plants newbuildings are stagnant.

LikeLike

I’m fairly new to the uranium market, but when speculating on a sustainable future spot price, what are those speculations based on? Why $80? Or $60? Or $100? Looking back before 2007-2008, the spot price was much lower. What’s different now? More power plants in use? Thanks for a great write up.

LikeLike

I prefer the Energy Fuels debentures listed on the TSX under EFR.DB (likely even more undervalued because American retail can’t buy them). They are convertible at C$4.15, while paying an 8.5% coupon (higher at significantly higher uranium prices) and maturing in Dec 2020. All while trading under par at 98.04 (last trade). It’s nice to be higher in the capital structure, get paid to wait and have access to the potential multibagger.

Anyone else own these?

LikeLike

Hammer, didn`t understand your point that UUUU better (vs UEC eg) if you expect U big price up movement is 1 year away. Thought UEC was a riskier bet (one more dependent on price upturn sooner) given their (I think) worse financial position than UUUU. Could you elaborate a bit on this, please?

LikeLike

Hi Angel, since the write-up Energy Fuels’ financial position has improved and there is less risk of a worst case scenario bankruptcy. Partly because of the equity raise of USD 16 million (working capital = about 18 months of run rate last time I calculated it back in June) but also because vanadium has kept rising so that in my estimate Energy Fuels may be able to generate enough profits from that in the coming two years without depleting working capital while waiting for uranium prices to turn.

My point then was that I believed there was a higher chance UEC could raise capital in bad times due to their share holder base and because their run rate is lower (about USD 20 million vs USD 30 million for Energy Fuels). Right now it is UEC that needs to raise capital very soon while Energy Fuels likely won’t need it to survive.

LikeLike

Thanks hammer. Yes, it seems the situation now is totally different, UUUU being the strong man and UEC the weak one. And UUUU even made a profit in the last quarter, though that won’t last I guess, given their guidance for Q3 and the weak contract deliveries expected. But things may change very rapidly in this sector!

LikeLike

Hello, what dou you think About Denison mines? Regards

LikeLike

Hi Luis, I don’t have a clear cut view on the exploration plays as I feel unequipped to value them correctly. My focus so far has been on companies with mines that have been producing in the past. That way there is less risk of “a hole in the ground with a liar on top”. That said I like the track record of both Lukas Lundin and David Cates and I haven’t ruled out investing in them at some point.

LikeLike

Could Energy Fuels sell uranium in the spot market. Have a feeling they will always produce somewhat to get cash flow. And uranium clean up work opportunities and alternate feeds their cash flow ability looks good to me. Vanadium production also makes it a diversified uranium producer. I think the last time they produced vanadium, it was in around 2013-2014. And their stock around that period went high up to around nearly 11 dollars. This stock may have more risk than say an etf that can spread your risk. But Energy Fuels seems like a stock a uranium speculator needs to own. There are risks though of course. Stocks go up for all sort of reasons, I just hope they can keep making revenue and cashflow..

LikeLiked by 1 person

Curious, has your view changed much on energy fuels and section 232 with a few weeks away?

LikeLike

Hi Hayden,

Here is the answer I gave to another reader a few moments ago. Of course these are only my opinions and I could be misreading the situation:

Well it is hard to say whether the overall risk/reward is better but I definitely think that both the risks and the reward are higher now than back then (for the reasons given below) and in that type of scenario I want to reduce my exposure somewhat so I have taken a bit off the table in recent weeks. Still a very significant position though.

On the positive side, those that are close to the process are more optimistic on 232. Cameco’s CEO has said he expects something to happen, among others. Also their cash position is healthier now than I would have expected at this time but much of it is due to dilution. They don’t need money in the immediate future + vanadium may buy them an additional year or two. Unless 232 goes through and they need to expand rapidly but that will be a positive problem then at the share price will be higher, so less of a concern.

On the negative side is that the UUUU share price is about 60% more expensive than back then while the uranium spot price has trended down in the recent month, as has the price of vanadium, so some of the fundamentals are in question. And still the share price has gone up recently which leads me to believe there is an element of Fear Of Missing Out. If that is correct then there will be more wanting to sell if 232 doesn’t go through so the reaction could be hard. This is just speculation of course and longer term I like their prospects. I think uranium will trade higher than $45/lb two years down the road no matter what happens regarding 232 – but I could be wrong.

LikeLike

While I agree that the overall risk/reward may be less attractive, I still think it skews heavily towards the reward. I agree that a negative 232 decision will most likely hurt them bad, but do you really think that effect will be more than really short term? Are there any other better plays to divert money to betting on a positive 232? Even with their increased share price?

LikeLike

I agree with everything you say here, Dick. I can’t find many uranium names that can compete with Energy Fuels in investment attractiveness, which is why about 25% of my uranium exposure is in this name. The main reason I have withdrawn some of my exposure has more to do with my general philosophy when it comes to bet sizing which is that when risk increases I will take chips off even if the risk/reward is the same (ie even if the reward has increased – if that makes sense). Back in the April to June period there was less risk of getting hurt due to the low share price and rising fundamentals. And less than a month ago you could buy this stock at a 20% lower price than now while the fundamentals (U and V price) looked more attractive. But I am on the same page as you when it comes to the reward. I think the odds are better for a positive 232 outcome than it was 10-12 months ago = higher reward and higher risk. But in my world those situations require lower bet sizing. If you theoretically could find say 20 uncorrelated bets with the same risk/reward profile as this one, I’d be all over it with the majority of my capital. But in just one name I think one has to be more careful.

If 232 is negative I also suspect there could be an exaggerated downside reaction short term that can turn out to be an opportunity. We’ll see. Exciting times ahead in the coming 12-24 months in the U space, that is for sure.

LikeLike

It has been a couple years since you reviewed Energy Fuels. I’m curious to know what you think now. They have diluted their investors a lot and again renewed their ATM this week for next year, somewhat disappointing. Now that Section 232 is behind us and it appears Uranium stocks are awakening as a sector, how would you compare the more diluted, but debt free, Energy Fuels with others in the sector? Would you change your analysis now? Are you still heavily invested?

LikeLiked by 1 person

I haven’t looked into it in detail recently but unless the rare earth thing has substantial value it seems to me a riskier proposition now given the combo of the higher share price, the fact the U3O8 price is still way below what they need to start production and as you mention the heavy dilution along the way (not a fan of how they did it either).

I sold the majority of my position in Dec 2018 when vanadium prices collapsed and the rest in August of this year when the URA etf was a forced buyer, unfortunately in hindsight. With U3O8 prices where they are at + the recent run up in share prices I’m only comfortable with the physical funds at this point. It remains to be seen if that approach is overly cautious.

LikeLike