A couple of weeks ago I had the honor of being a guest on my current favorite investment podcast, The Mike Alkin Show. On it we discuss why the contrarian approach can be a profitable one and why so few investors are comfortable with it, how my 12-year poker career has affected my view on investing and we also touch on mistakes I have made in my investing career so far. I will dig deeper into this last part in a future post because I think there are some lessons to be learned – especially on what not to do!

Mike has done a ton of deep work on the uranium sector and is probably the person with the most knowledge on the current supply/demand & inventory situation in the space. And I am quite vocal on my findings on individual uranium companies on Twitter, on YouTube and on my blog. So that is how we connected on Twitter.

An example of how I generate investment ideas

As Mike has played a role in my uranium education and since many people have asked me how I generate investment ideas I thought this would be a great segue into how uranium initially caught my interest and perhaps an example of how one can go about turning a fuzzy idea into a possible investment. (Note that this post is only meant to be an example of the initial stages. It won’t cover the work on individual companies as that would be outside the scope of one article)

How Xi Jinping showed me the light in a roundabout way

In early January I was looking around for new investment ideas and thought Xi Jinping’s speech to the 19th Party Congress could be a starting point. Those are held every five years and they have all been fabulous at predicting what was to come. When Chinese leaders decide on a long-term idea they are able to follow through, unlike in a typical western democracy.

So who are these speeches aimed at? Probably first and foremost the leaders out in the municipalities throughout China. If they don’t listen to what the President wants and then implement his wishes they will be out of a job. So it gets done.

From GDP growth to blue skies again

What was interesting about this particular speech is that whereas previous five-year plans have focused on GDP growth at all costs this speech had a different focus in that the environment is mentioned again and again and a recurring theme is how China needs to ”make our skies blue again”. The Health Effects Institute estimates that more than 1.5 million die from air pollution in China.

Deciding on an investment theme

So I started thinking about how an investor can approach this shift. How can China make the transition from dirty coal to cleaner energy sources? Initially I thought liquefied natural gas, LNG, was the play. Recent activity certainly suggested this was a good idea as China had increased their imports from 2016 to 2017 by a whopping 50%!

On top of that, Japan, the largest importer of LNG in the world, had held the course while most analysts had expected Japan to decrease their imports.

But as I started looking deeper into it both of those factors turned out to be warning signs, at least that is how I viewed it. It turned out that China was experiencing bottle necks due to the sudden increase. Their infrastructure couldn’t keep up which might lead to a slowdown, I thought. So that was one risk.

From liquefied natural gas to nuclear power

Another issue came up when I started looking into why analysts expected Japan to decrease their imports and that was related to the Fukushima accident which brought down all of Japan’s 54 nuclear reactors. Most of those were expected to come on soon after but it wasn’t happening at the pace everyone thought it would due to constant court delays. But since it seemed to be a question of time the whole LNG idea started to seem more risky to me and it warmed me up to the idea of nuclear power. And one thing I didn’t initially understand was that LNG wasn’t THAT much cleaner than coal. On an index where coal is at 100, natural gas is at 45. On that same scale nuclear energy is somewhere between 0 and 1! Time for the left to wake up to this fact…

Introduction to uranium in late 2016

A fellow Swedish value investor, Kenny Granath, had alerted me and my investing network to the idea of uranium/nuclear power as an investment theme back in late 2016.

Kenny worked in the nuclear industry so his words obviously carried extra weight due to that fact alone. But not only that, he had shown an ability countless times via his blog to do deep sector analyses in a way I hadn’t seen before from individual investors and those posts were the initial inspiration behind my investment blog in 2014.

But he also said it was probably too early to enter the uranium space as production cuts and consolidation had been minimal at that time and for that reason I simply made a mental note of it but never took a closer look.

CO2 emission quotas explode

I started doing just that in January after having discarded LNG. The climate was increasingly on the agenda and the price chart for CO2 European emission allowances were making some big moves, which had increased the price of electricity in Sweden, and which in turn had renewed my interest for Swedish wind energy companies.

Swedish nuclear power had been on the retreat since 2014 when the owners decided to close down four of their ten remaining nuclear power plants due to the low price of electricity. I had been following the electricity space and the political discussions quite closely since then and my impression was that the owners unsuccessfully had tried asserting pressure on the Swedish politicians to give compensation for delivering baseload energy.

But things have been changing lately and the idea of building new power plants further out in the future has started entering the discussions, so while I knew nuclear was struggling I also knew that it was far from dead in the west. And so after LNG was dropped as an investment idea I started looking closer at uranium.

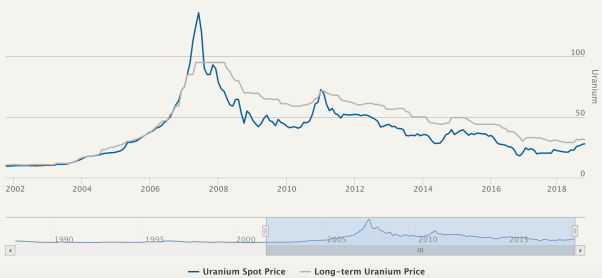

The uranium price chart from hell

Being a deep value guy a price chart like the above is interesting. The first thing I usually do when a sector peeks my interest is to read the annual reports of the biggest companies in the industry, initially at least those parts give a sector overview. That meant I started with Cameco and what struck me immediately was their mentioning of the fact that the price of uranium was way below the marginal cost of production, as could perhaps be expected by looking at the graph.

Obviously that cannot continue indefinitely so the next step is to look into what has been the cause of it and what may trigger a change to a normal pricing environment where the price returns to equilibrium, ie slightly above the cost of production.

The cause of the bear leading up to 2004

Historically uranium has had these extremely long bear markets that makes your stomach churn. The bear market that proceeded the current one was mainly due to downblending of atom bombs from the former USSR and the US creating the equivalence of a gigantic mine that simply destroyed the market.

The cause of the upwards explosion

Then in about 2004 China started getting interested in nuclear power and due to flooding in some large mines that were supposed to come online this created a squeeze on both the supply and the demand side. The long bear market had made exploration unattractive so when demand started showing up suddenly there was fear there wouldn’t be enough uranium available which along with financial players rushing in created the panic that can be seen in the chart in 2007 and so the price overshot by a large margin.

When financial players started liquidating their holdings, partly due to needing funds in the wake of the financial crisis, the price came back down do equilibrium like levels, which is to say slightly above the cost of production.

The cause of the bear from 2011: Fukushima, Kazakhstan &…???

Then in 2011 the Fukushima accident happened which made Japan decide to close down their reactors for review. At the same time the production from Kazakhstan had increased at a pace no one saw coming from 10% to 30% of global production in only 4 years.

In more normal liquid markets the price would be hurt by such a squeeze but it would also quickly correct after the marginal players had been knocked out. This wasn’t happening and in the first weeks of research I didn’t really get a firm grip as to why even though I had read the reason in Camecos annual report and had seen the graph that explained it. For some reason the significance just didn’t register.

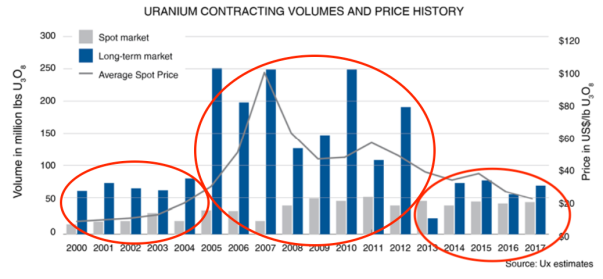

It’s the long-term contracts, stupid!

So I started looking for other views on the sector and for that Real Vision is often top notch. This is a subscription-based financial media service where people who have dedicated large parts of their lives to understanding a particular field are being interviewed in long-form. I have spent countless hours as a fly on the wall during my daily long walks with my dog listening to world-class experts in different areas. And here I found two excellent presentations from Mike Alkin of Sachem Cove and from Adam Rodman of Segra Capital that really hit home the point that was right in front of my nose:

Long-term contracts fixed at high prices during the good years were the reason the miners weren’t dying and killing off supply!

The above graph is the primary reason why uranium is in the state that it is in. And it is also the reason why I pulled the trigger and started investing in uranium now rather than wait.

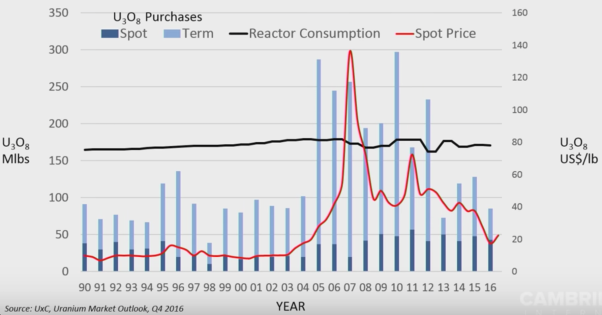

Once one knows that annual demand is in the 170-180 Mlb range then it becomes only too clear what is going on. And as can be seen below where demand is included in the picture, it is a very constant thing in that business. It doesn’t jump up and down along with the general market cycle.

I would spend a few minutes studying the graph below, which is essentially the same as above but with demand added in. Note that the numbers on the right side, the price, is only applicable for the red line. For all other information, the volume in millions of pounds (Mlbs) is the reference. What the graph tells you is that from 2005-2012 the contracted volume was way above annual demand so the decline in price from 2012 should come as no surprise, especially when factoring in Kazakhstan and Fukushima as well. Those contracts are now rolling off and new ones will have to be signed in the coming years and it will be done at prices that are above the cost of production, which is at least north of $50/lb.

A new Fukushima = a new bear?

And by the way, that graph is also the main reason why I, unlike most people who follow the space, am less concerned with a new Fukushima type-accident knocking down the price of uranium.

People have a tendency to equate Fukushima with the bear market and forget the Kazakhstan and the contracting situation. But we are in a completely different place now with regards to those last two factors so I don’t think you can simply point to the accident and say that the last time it happened can be a road map for how the price of uranium will develop. Unless the world decides to dismantle nuclear power once and for all following such an accident. But then what happens with the climate change push that is really taking a hold on the world now?

So in the unlikely event an accident happened tomorrow my money is on a scenario that says the price is higher two years from now, after an initial dip.

A shout-out to true environmentalists

As an aside, now that I am on the topic of safety: There are some so-called environmentalists out there that need to examine their real motives when speaking out against nuclear energy…

The question is: Are you concerned with saving lives in the real word, or are you more concerned with the idea of pressing on a topic that gets you a knee-jerk hug from do gooders who do no good? Because an anti-nucIear stance will certainly give you that quick gratification of the warmth of the crowd.

Let’s say you agree coal has to go but that nuclear is no option. Electricity from wind and solar tends to hit the grid all at once, or not at all. So what to do at those times when the weather doesn’t behave? Pray?

Great article, was wondering your thoughts on the incoming correction expected to hit the markets as a whole and its possible effects on the uranium space. If it does come sooner than later would that have any affect on spot price? or just affect on the equities themselves?

LikeLike

Michael, I think it will hit the equities (initially) but not the spot price. In other words, it doesn’t concern me and it is one reason why my exposure to uranium is high.

LikeLike

What makes you so sure that a correction is coming on top of what already happened?

Anyway, I can think of few stocks that would be less affected than uranium stocks. These are mostly small and micro caps, already beaten down over the years and there is not much interest and ownership among larger institutions except for some specialized commodity funds, but shouldn’t exactly these do well when the stock market corrects (be negatively correlated)?

The Spot price shouldn’t be affected at all. It is determined by traders (okay and Cameco/physical holding funds) and these shouldn’t care about the valuation level of the market, they trade up and down if they know their business well.

LikeLike

I doing some research on Uranium producers and am trying to better understand the production costs per pound or kilo of the big players. I like to protect my downside, so important to me that a company has a low cost position and the financial dexterity to withstand prolonged downturns — even as all signs point bullish.

Have you found any resources to be very helpful in this regard?

Company specific, Cameco has my attention, but I don’t want to buy a company that can get its butt kicked by Kazatomprom when push comes to shove. Also, I’m worried about the depletion of their legacy contracts that they’re getting substantial cash flow generation by fulfilling them at spot prices…. a tide that will turn severely against them if they were still writing long term contracts over the recent path.

I appreciate any guidance and would love to connect over email. Cheers.

LikeLike

Hi Andrew, if you want the best downside protection go for Uranium Participation or Yellow Cake plc. None of those are miners. They simply buy and hold uranium and both of them at trading at very attractive discounts right now which I don’t think will continue going forward. I would personally have no issues with shoving large amounts of capital into those two and I would sleep very well at night.

If you want a miner that is almost as safe Cameco is the only option imo. I don’t understand what you mean by the following: “I’m worried about the depletion of their legacy contracts that they’re getting substantial cash flow generation by fulfilling them at spot prices…. a tide that will turn severely against them if they were still writing long term contracts over the recent path.”

Their situation is such that they are making money on those contracts by buying in the spot market and pocketing the difference. As spot rises so will the value of their contracts, so there is no big threat there. Also, in my opinion Kazatomprom is less of a threat than the non-transparent inventories. Kazatomprom has limited levers if they really wanted to flood the market, which they probably wouldn’t anyway even if they could now that they are listed and answer in some shape or form to shareholders.

You are welcome to connect via PM to @hammerinvesting on Twitter for my email. I prefer not to have search engines sniff my email on here.

LikeLike

Many thanks for all interesting articles on your blog!

I understand that you invest full time – is that correct? If so – how do you structure your time? Regular hours? Keep track of your progress?

/Martin

LikeLike

Hi Martin, thanks for the compliment. I am glad you enjoy the articles on here. I can tell you they often take much more time to plan and to write than I expect when I get the initial idea…

Structure? That is a great question and one I often struggle with. I put in more than my fair share of hours but do I work in a linear fashion for all of those hours like a Warren Buffett who is reported to read 500 pages every day? Truthfully no. I often wish I could do that but I have tended to work more like many artists, which is to say I will have a strict plan and work long 12+ hours for a period and then have another period where I need a break to recover where I am all over the place and not disciplined at all jumping from one thought and one piece of info to the next.

To offset that I do lots of walking on the beach every day, between 1 1/2 to 2 hours usually. I think that is an underrated activity that has a lot of mental benefits, besides the obvious physical ones. I use that time to listen to audio books, real vision interviews, podcasts and just to structure my thoughts on investments in general. I will usually put in the deep work activities prior to the walks, although I am not always super smart about that. I also throw in kitesurfing sessions when the wind is there and then usually work in the evening in those cases.

This may not be the optimal way to go about being your own boss and perhaps not the recommended way either. But I am hesistant when it comes to changing a formular that has been winning above my expectations since 2005. But I also realize that if the world was full of Buffetts reading 500 page of 10Qs every day it would be questionable if there was room for my approach.

Are you considering going at it full time or perhaps you are already doing that?

LikeLike

Thank you! That was really helpful!

I have just deciderat to quit my job at a large company as I find too much of the time there is wasted on ”low return” tasks like administration and internal politics. For many years I have been investing my own money in my spare time.

My plan now is to split my time between doing some consulting and invest my own money. Your answer gave me some great input as I need to find my way to use my time efficiently and also handle the social bit of it, which is the main reason for why I plan to do consulting for maybe 25-50% of my time.

I really think that activities like long walks and kite surfing – being a fair amount of time outdoors is a really good idea. Have you had this way of working since you started or made any major adjustments since you started?

/Martin

LikeLike

Congratulations on making the leap, Martin. Hope it works out to your satisfaction. It is in many ways a free and very fullfilling way to spend your time.

The social bit is probably the most challenging aspect of investing full time so I can see why you want to hang on to consulting for that reason. Eating lunch at the local restaurants is another small way of decreasing the isolating aspects of investing. It may sound unimportant but it really can make a difference.

Additional streams of income could also prove extremely important to keep the pressure at a healthy level, especially when dealing with years when your portfolio is not performing as you would have hoped. I personally don’t have that anymore as I quit poker very recently after a nice three year streak in investing. But frankly it is an uneasy feeling and I think one has a higher chance of staying rational with additional streams of income. Just my 2 cents.

LikeLike

Thank you! Many good points. I am also planning to do a lot of work from the nearby library.

/Martin

LikeLike

Hammer, it’s been a while since you posted your great analysis on Energy Fuels. Has anything changed, negatively or positively, in your view of this company? You gave a 12 month warning if the price of uranium doesn’t go up above $45, concerns of bankruptcy or dilution. We are only a couple months away and it seems unlikely the price of uranium will get to those levels. Also, how do you perceive the downside risk on EFR if the 232 decision goes against them. Thanks.

LikeLike

Hi Canadian,

Well it is hard to say whether the overall risk/reward is better but I definitely think that both the risks and the reward are higher now than back then (for the reasons given below) and in that type of scenario I want to reduce my exposure somewhat so I have taken a bit off the table in recent weeks. Still a very significant position though.

On the positive side, those that are close to the process are more optimistic on 232. Cameco’s CEO has said he expects something to happen, among others. Also their cash position is healthier now than I would have expected at this time but much of it is due to dilution. They don’t need money in the immediate future + vanadium may buy them an additional year or two. Unless 232 goes through and they need to expand rapidly but that will be a positive problem then at the share price will be higher, so less of a concern.

On the negative side is that the UUUU share price is about 60% more expensive than back then while the uranium spot price has trended down in the recent month, as has the price of vanadium, so some of the fundamentals are in question. And still the share price has gone up recently which leads me to believe there is an element of Fear Of Missing Out. If that is correct then there will be more wanting to sell if 232 doesn’t go through so the reaction could be hard. This is just speculation of course and longer term I like their prospects. I think uranium will trade higher than $45/lb two years down the road no matter what happens regarding 232 – but I could be wrong.

LikeLike

Thank-you for your thorough response! Very much appreciated. What isn’t clear to me is whether we’ll hear what the DOC recommends on 232 as soon as mid April or if they keep it confidential in passing their decision to the president and we wait another 90 days beyond that (as they’ve done with the Auto decision on 232, which was passed to Trump mid Feb and still isn’t public). I agree, a negative decision on 232 could hurt a lot in the short term at least.

LikeLiked by 1 person

That is not clear to me either. I have assumed the DOC report would be made public when they conclude their investigation but maybe that isn’t so in which case we may have to wait until mid July.

LikeLiked by 1 person

Today the CEO of Cameco commented on a Japanese utility selling 115,000 lbs of uranium into the market and seemed to suggest this could be a possibility from other Japanese utilities. On its own that one company doesn’t seem significant, but have you heard of this potential for other Japanese companies?

LikeLike

No, I haven’t heard anything about that except what you mentioned.

LikeLike

Thanks again for an insightful article!

Can I ask what is your opinion on investing in uranium via ETFs (well, mainly Global X Uranium)? I would think that ETFs could offer a bit more protection than, for example, picking just one company.

LikeLike

Thanks for your kind words, Willie!

In theory investing in Global X Uranium (URA) sounds like a great idea to diversify but in fact it is a terrible, terrible idea because this ETF buys and sells at the exact wrong times which is something I and others have benefitted tremendously from. In fact I suspect I owe a lot of my performance in 2018 to this ETF because it made it possible for me to pick up shares that this ETF had thrown out indiscriminately of the price.

A second reason not to invest in URA is because they recently made a decision to transition into “nuclear components”, ie. non-uranium miners as well, so it is very far from a pure play.

What I’d do if I didn’t know much about the micro about a sector is buy a basket of 6-7 names consisting of 4-5 of the bigger market cap names (Uranium Participation, Cameco, NexGen, Energy Fuels, Kazatomprom for example in the case of uranium) and then have perhaps 2 small explorers, which are much more risky, to go on top. Equal weighting. And then forget about it for 3 years and accept whatever happens. I suspect such a strategy would do well. This shouldn’t be considered investment advice by the way, just what I’d probably do if I was in that situation and what I’d do if I wanted to invest in a sector but don’t have the time to investigate individual names. Another option is the Geiger Counter ETF. They have a pretty solid approach. Personally I just always avoid ETFs because I hate fees and would much rather pick a number of stocks in a sector completely by random. The more diversification you crave, the bigger the number. Personally I don’t think there is a need to go beyond 10 names in order to achieve acceptable diversification.

LikeLiked by 2 people

Really appreciate your response! I noticed that I should have read your older entries again for a memory refreshment. It’s apparent from your earlier writings – and videos – that Uranium Participation is probably the best bet for a risk-averse investor to invest in uranium. And, its share price seems to on the same level as, for example, a year ago.

LikeLiked by 2 people

Excellent article Hammer! I really enjoyed the way you broke that all down; thank you for taking the time to write this. Your English is superb!

LikeLiked by 1 person

Thanks Dieter!

LikeLike

Today, as part of conversations with the Canadian PM, Trump discussed steel and aluminum. “They also discussed China, uranium, and the new NAFTA”. No details given of course, but this suggests to me that Trump is going to do something with 232 for uranium. If the report given to him had just suggested the status quo or if Trump’s response to the report was going to be the status quo, i can’t imagine any reason for uranium to be the topic of conversation with the Canadian PM. Seems logical to me to conclude that something must be coming, just a matter of what it looks like. I was surprised not to see Energy Fuels and URE move on this news, but maybe i’m the only one reading into it this way. 🙂

LikeLiked by 1 person

Thanks for your thoughts, Canadian. You could be on to something here…

LikeLike